2020 ushers in a new Space Race, and this time it’s private

Posted 27/01/2020 by Pedro Pires

It’s now more than fifty years since man’s first landing on the moon. While the past five decades have seen a wealth of innovation and scientific progress, the space industry has yet to match the dizzying heights of 1969’s Apollo 11 mission. Today, outer space remains the Final Frontier. But for how long?

After many quiet years in space (figuratively and literally), the industry is once again starting to make some noise. With investment returning to record levels, there’s talk of a new Space Race fast approaching. But things are a little different this time around.

The real Star Wars

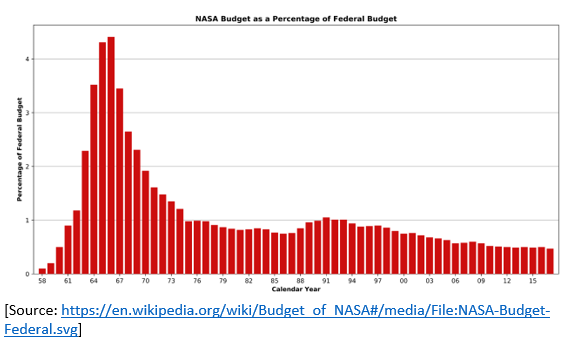

The previous golden age of space played out on a dramatic stage, back-dropped by the icy developments of The Cold War. The 1950s and ‘60s saw a colossal increase in public expenditure on space technology which represented far more than just a scientific revolution. The Space Race marked a display of political strength, innovation, and endeavour – a kind of proxy battle between the world’s two great superpowers.

The heady Space Race was to reach its peak with the Apollo 11 mission in 1969. From there, things lost momentum in the public sphere. After a handful of successful moon landings, several unfortunate incidents, and the eventual de-escalation of the political stand-off which sparked it all off, space funding returned to normal levels in the mid-70s.

A race re-ignited

For the first time since the 1970s, space expenditure is today back on the rise. But this time it’s not governments splashing the cash. What we’re seeing is a huge surge in interest from the private sector, pushing the development of new space and aeronautical technologies.

Crucially, this shift to the private sector means it’s no longer a two-horse race. The New Space Race boasts a far more diverse range of competitors, this time from all over the globe.

Where private capital was once almost non-existent in the sector, it now reigns supreme. From 2000-2015, a total of US $13.3bn of investment finance flooded into the space sector – $2.9bn of which came from venture capital financing.

2015 saw market giants like Google and Fidelity Investments sink $1bn into SpaceX – the company responsible for the Falcon Heavy Reusable Rocket, and the Starship launch vehicle. Neither project received a penny of government financing. Other big players in the market include Blue Origin (Amazon), Rocket Lab, Virgin Galactic, ULA (Lockheed Martin and Boeing), and EADS (Airbus).

And we’re still on an upward trajectory. The likes of Morgan Stanley, Goldman Sachs, the Bank of America, and UBS are all conducting regular research on the industry’s growth. What’s currently estimated to be a $400bn space economy is projected by Wall Street to become a multi-trillion-dollar economy in the next 10-20 years.

What’s behind the sector growth?

Well, primarily it’s cost. Where space had become expensive in the years immediately following the Cold War, the introduction of the private sector has driven prices down, thanks primarily to increased competition and innovation.

SpaceX has been at the forefront of finding low-cost solutions. In 2013, the published cost of their Falcon 9 rockets hit just $56.5m per launch. This represented the most competitive launch on the market to date.

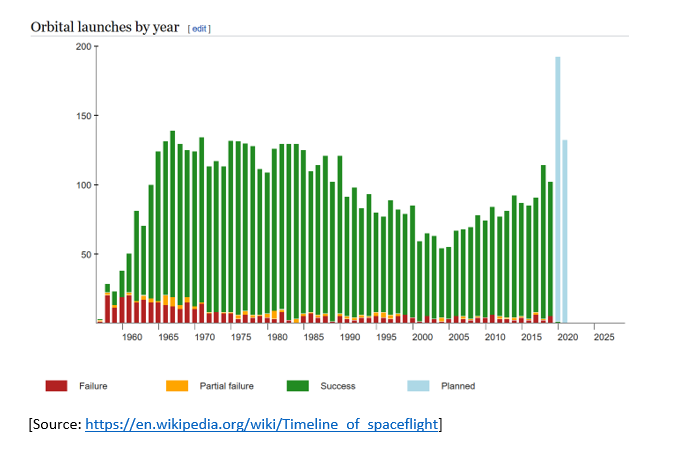

As a result of these falling costs, 2018 saw the number of space launches surpass 100 for the first time in almost 30 years. This is territory we haven’t seen since the days of the Apollo missions.

The industry isn’t just growing. It’s changing, too. The lowered cost and shift to the private sector are having a significant impact on the shape of the industry. Today’s picture is based less on the balance of competitive nation states, and more on commercial enterprise. In a sense, a metaphor for the times.

Greater competition has driven down price, but it’s also lead to greater innovation. Re-usable tech sits at the heart of lower costs. Robotics are also making maintenance and replacement of satellites far more cost-effective.

Exploration was the stated goal of the Cold War Space Race. While this remains a significant factor today – Musk (Founder/CEO of SpaceX) famously hopes to die on Mars – space tourism and commercial interests are also playing substantial roles.

Commercial space flights are now very much a reality, being led by the likes of Virgin Galactic. There’s also a large crossover with satellite-related communications businesses. Companies like ViaSat, Intelsat, and Loral Space & Communications all focus on internet services provided by large satellites, orbiting the earth at a fixed distance to offer improved coverage. Iridium Communications – which offers a variety of mobile communications services – are set to complete a $3bn network of satellites. In other words, it’s a busy market.

The numbers show that this is an exciting time for space. As we enter a new decade, we seem also to be entering a new Space Race. If so, it’s sure to be a very different race to last time. Less tension (we hope), but equal levels of excitement. With more diverse streams of investment, and a broader array of challenges, there’s no telling what’s possible for the next decade of space exploration. And there’s no doubt that it will be one of the most pioneering sectors of the 2020s.